- categories: Linear algebra, Factorization

Definition

The Singular Value Decomposition (SVD) of a matrix is a factorization of the form:

where:

- is an Orthogonal matrix whose columns are the left singular vectors of .

- is a diagonal matrix with non-negative real numbers, called singular values, arranged in descending order.

- is an Orthogonal matrix whose columns are the right singular vectors of .

Construction

SVD is derived by observing the properties of and :

- and are symmetric and e.

- These matrices can be eigen-decomposed as: positive semidefinite

where is a diagonal matrix containing eigenvalues. - The singular values of are , where are the eigenvalues of or .

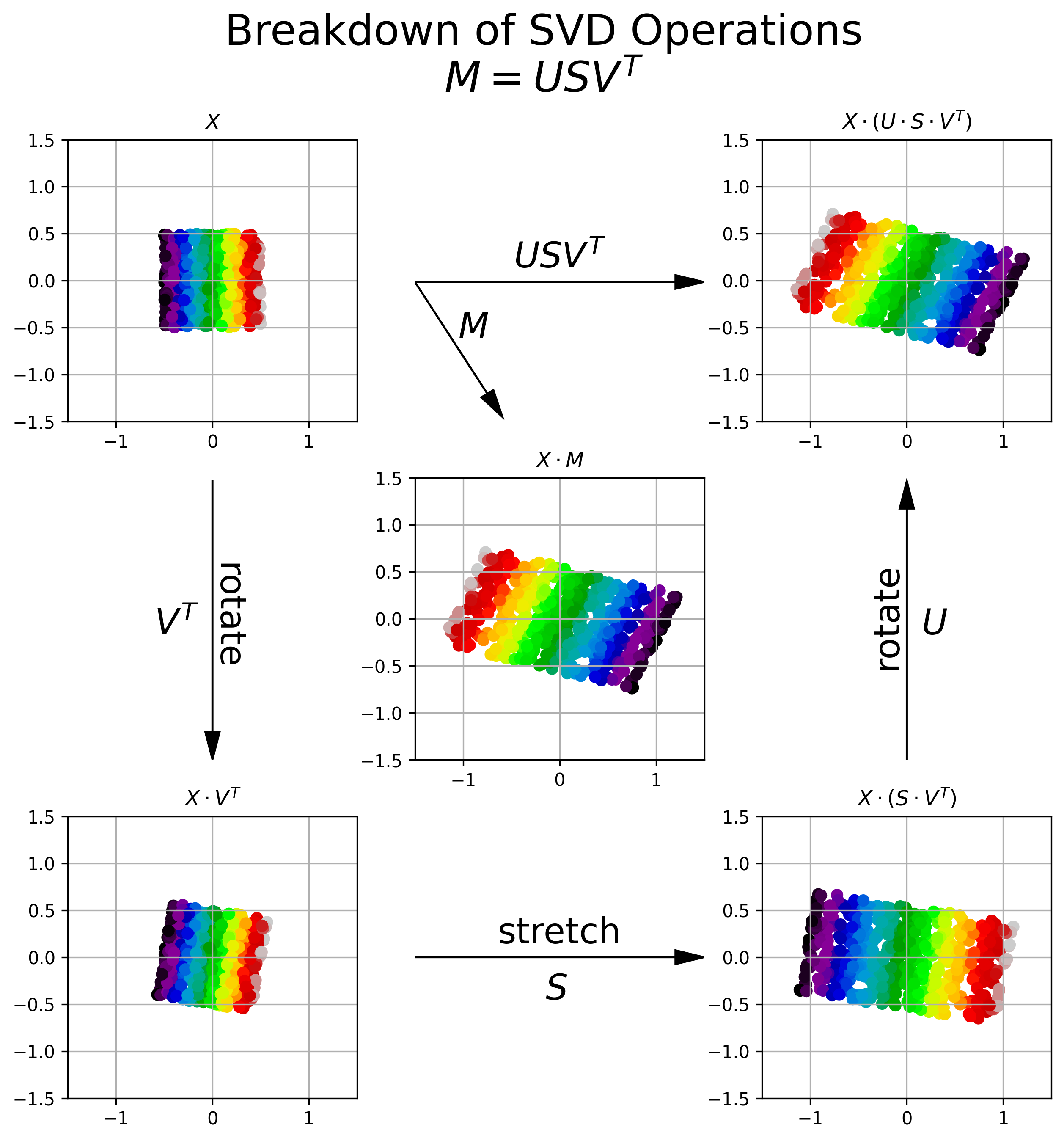

Intuition

The SVD of a matrix can be thought of as a sequence of linear transformations:

- Rotation (via ): Aligns the data to principal directions.

- Stretching/Squashing (via ): Scales the aligned data along principal directions.

- Rotation (via ): Maps the scaled data to the target space.

Key Properties

- Singular Values: The diagonal entries of are the singular values .

- Rank: The rank of is equal to the number of non-zero singular values.

- Norms:

- (Frobenius Norm).

- (Spectral Norm).

- Relation to Eigenvalues: The non-zero eigenvalues of (or ) are the squares of the singular values of .

Applications

- Dimensionality Reduction: Core of principal component analysis (PCA).

- Image Compression: Approximates images with low-rank matrices.

- Recommender Systems: Latent factor analysis in collaborative filtering.

- Numerical Solutions: Solving Linear Systems, pseudoinverse computation.

- Data Science: Low-rank approximations for noise reduction.